Putting the Success in Succession Planning and Management

by Romel Bonilla, Supervision Manager, Supervision and Regulation, Federal Reserve Bank of Chicago; Joel D’Souza, Senior Examiner, Supervision and Regulation, Federal Reserve Bank of Chicago; and William Mark, Lead Examiner, Supervision and Regulation, Federal Reserve Bank of Chicago

Banking industry regulators consider proactive succession planning and management a key governance tool in promoting a bank’s resilience in difficult times. Competent succession planning addresses the evolution of a bank’s business strategy in the context of its management structure. Therefore, succession management is the implementation and maintenance of a plan that should reflect a thoughtful distribution of roles, responsibilities, and approval authority for a management team. Regardless of the degree of formality, an effective succession management program is composed of the primary components of dynamic planning and diligent ongoing management. However, when management succession plans are neglected, organizations are often unprepared for the loss of key employees.

While turnover is inevitable, unexpected occurrences can instill uncertainty and turmoil in any management team, particularly if a succession program is dormant. Thus, when a key member of management leaves, the bank is more reactive than proactive in addressing the staff vacancy. Proactive preparation is essential in effectively managing staffing vacancies. An active succession planning process, which includes a deliberate development and cross-training focus, is the foundation for successfully addressing both planned and unexpected staffing changes. In many cases, operational disruptions arising from the loss of any one individual are mitigated as much as possible when there is already a successor identified or when a bank has existing “bench strength” and staff is prepared to assume the day-to-day management responsibilities, even on an interim basis.

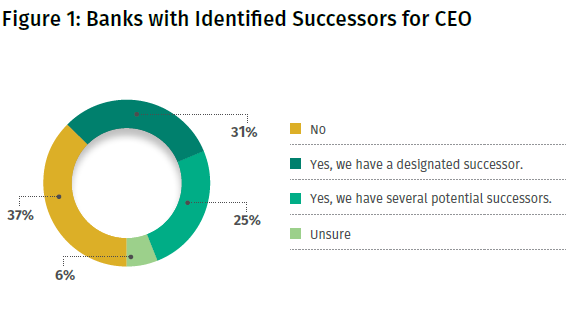

In the banking sector, the importance of identifying, developing, and maintaining qualified management is supported by several industry trends in the composition of community bank management teams. Bank Director magazine’s 2019 Compensation Survey of bank executives and directors conducted by Compensation Advisors in Newtown, PA, noted that, among the respondents, CEOs have a median age of 58 and about one-quarter of community banks (i.e., banks with assets totaling $10 billion or less) projected their CEOs would leave, through retirement or otherwise, over the next two years.1 Meanwhile, as denoted in Figure 1, over 40 percent of the respondents did not have a successor or potential successors for the CEO role or were unsure if any had been identified.2

At smaller banks, the depth of talent readily available in-house for key management positions is typically limited. In contrast, larger banks usually have a deeper talent pool to consider for successors. More formal processes to identify development needs and prepare candidates for various leadership roles are appropriate for all banks, but to what extent depends on the asset size, complexity, and culture of each institution. Community banks regularly face strong competition for skilled, experienced staff who are committed to the community bank business model. Tools such as relevant training programs and compensation strategies are typically needed to attract and retain staffing capable of fulfilling leadership roles. Commitment to a development program should align with a bank’s long-term business strategy and demonstrate to staff that the board of directors and management are committed to developing in-house talent. When properly crafted and communicated, proactive succession planning also helps a bank retain key employees.

Maintaining competent leadership at community banks often goes beyond the confines of the institution into its leadership role in its market footprint. Interactions with local businesses and municipalities may lead to business prospects for a bank and provide opportunities to connect with the local community to better understand market conditions and the community’s banking needs and, in turn, contribute leadership to the community. Of course, there is an additional supervisory benefit, as contributions such as leadership in community enrichment and development efforts are relevant factors when assessing the degree of compliance with the Community Reinvestment Act. At the 2019 Community Banking in the 21st Century research and policy conference, Federal Reserve Governor Michelle W. Bowman stressed the systemic importance of community banks to their local communities. She noted that “it is critical that we work together to find ways to preserve the benefits provided to communities by well-managed, strong financial institutions that are deeply grounded in the areas they serve — including the communities that they expand or merge into.”3

The Federal Reserve’s interests are aligned with state member banks to develop and maintain competent bank leadership. This article provides a brief overview of succession planning, including useful supervisory guidance, the benefits of such planning, and related banking practices observed by Federal Reserve examiners.

Supervisory Perspective

Supervisory guidance highlights the importance of competent management in implementing prudent risk management practices that identify, measure, monitor, and control current and evolving risks. These practices help an organization navigate changing business conditions and shifting organizational directions. Supervisors evaluate the depth of risk management relative to an organization’s risk profile, which, in turn, informs their supervisory focus. Effective risk management is a major factor that examiners consider in assigning satisfactory supervisory ratings.4 Accordingly, human capital is an integral part of risk management and strategic planning, and to be effective, succession planning and management is vital to the process.

As noted in the Federal Deposit Insurance Corporation (FDIC) Supervisory Insights publication, “even the smallest community banks can find ways to motivate employees and expand and diversify their skills through cross-training, serving on committees or special projects, attending conferences, and coaching and mentoring relationships.”5 To facilitate the continuity of a bank’s board of directors, the Comptroller’s Handbook: Corporate and Risk Governance by the Office of the Comptroller of the Currency (OCC) encourages the use of tenure policies to guide the retirement or replacement of directors through elements such as term limits and a mandatory retirement age to better anticipate the timing of leadership changes.6

When assessing the appropriateness of leadership at any banking organization, Federal Reserve examiners operate under a basic mantra: Does leadership exhibit relevant experience, display sustained competence, and demonstrate a high level of integrity? Each of these factors is meaningful when determining the effectiveness of succession planning as well as its importance in the overall supervisory assessment of management.

Challenges of Succession Planning

The benefits of a well-crafted succession plan are subtle but impactful. Smooth transitions of leadership, greater flexibility, and overall readiness to accommodate unexpected industry, economic, strategic, and personnel changes are invaluable. Proactive plans with a focus on employee development foster engagement and support recruiting efforts. Therefore, leadership development is a critical component of an effective succession plan to transition an organization through the disruption arising from employee turnover.7

Conversely, a lack of preparation for management turnover, whether expected or unexpected, can lead to naming a successor who lacks the requisite commitment, expertise, demeanor, or cultural fit to properly execute the duties of the position. During a period of turnover, a bank’s staff could even be distracted from the day-to-day business of managing the bank and thus potentially compromise the integrity of the internal control environment.

Practically, busy schedules and full board meetings can relegate succession planning to a lower priority. Because cultivating future management does take time, a board should assign greater urgency to planning and development efforts. From a leadership perspective, the potential negative ramifications of inactivity can be the greater motivator to ensure that succession plans are current. When succession plans do not address the bank’s current business strategy and staffing resources, the board and management may be unprepared for a key employee’s departure, which could stifle success in both the near and long term.

Developing a management succession plan can be challenging. For example, shifting local workforce dynamics and demographics can be big obstacles to finding and retaining qualified candidates. Due to the sensitive nature of management succession discussions, board and senior management will need to consider the legal and ethical concerns that may arise. Finally, because quite a few community banks are closely held family-owned organizations, the need for succession planning may be more urgent as senior leadership nears retirement and the next generation is uninterested in assuming a leadership role at the bank.

Responsibilities and Methods

Management succession planning is essentially a risk management tool designed to minimize the adverse effects of a change in leadership. A bank can craft a useful succession plan by considering the elements of the Federal Reserve’s risk management framework. The four elements of sound risk management are board of directors and senior management oversight; policies, procedures, and limits; risk monitoring and management information systems (MIS); and internal controls and independent review.8 The significance of “tone from the top” is paramount for employees to observe the board’s and management’s commitment to a sound risk management framework and succession planning to facilitate business continuity.

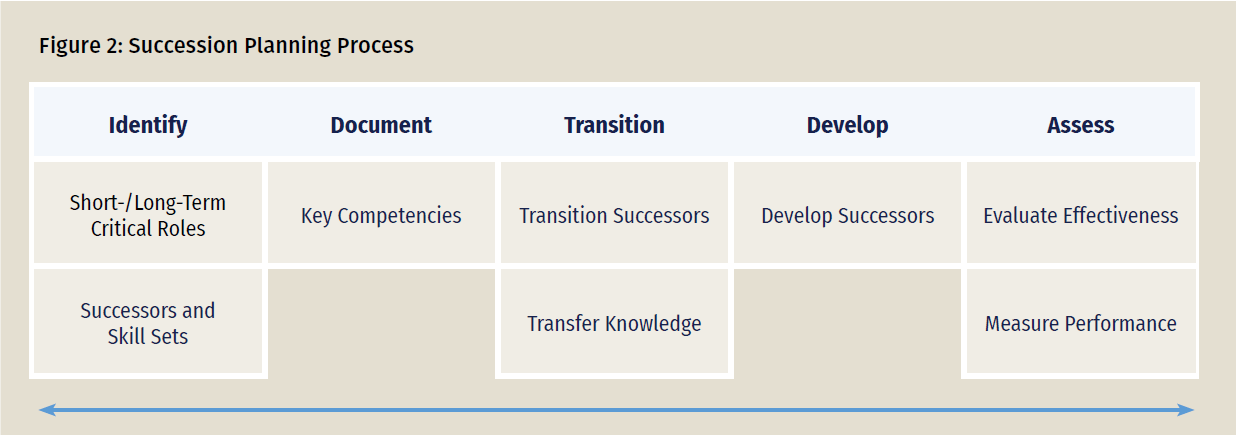

As effective succession planning supports viability and continuity of operations, a plan should be developed, maintained, and endorsed by the bank’s board of directors and senior management. Assuring the bank has competent leadership is one of the main responsibilities of any director,9 with the board ultimately responsible for ensuring “that senior management is fully capable of implementing the institution’s business strategies and risk limits.”10 In this manner, a board and senior management would coordinate the succession program with the strategic plan, business direction, and culture to establish actionable steps to identify and develop successor candidates. As highlighted in Figure 2, succession planning is a multilayered process involving a concerted assessment of the bank’s needs relative to resource and skill gaps, and an intentional focus on developing successor candidates, while promoting accountability through ongoing evaluation.

An established succession program helps ensure that the intentions of board and senior management are clearly communicated when appropriate, especially in times of tumult, while still mindful of confidentiality considerations. Building a succession strategy aligned with the strategic plan and centered in staff development supports business goals and promotes flexibility. A candidate pool for the various key management positions should reflect the use of a skill assessment mechanism to determine each individual’s readiness for a leadership position. As part of this process, a candidate’s strengths are identified to reinforce or complement organizational strengths or to address recognized organizational weaknesses. Skill sets are cultivated to account for a candidate’s lack of experience as well as to take advantage of recognized strategic opportunities or confront external threats.

Based on regular and discreet discussions, a bank’s board of directors can evaluate the management and staffing structure by summarizing ongoing reviews that measure achievements and professional growth toward established milestones and goals. Such discussions should be kept confidential given the sensitivity of the information. Access to independent sources such as consultants or trade organizations can provide an objective perspective on plans and strategies, staff skill sets, or even competitive compensation structures. Attention to the succession plan throughout the development, execution, and maintenance processes is stressed because, as noted in Supervisory Insights, “a well-designed plan may still fail if its implementation is inadequate.”11

Recruitment and retention are tied to whether employees believe that their professional potential is being developed and used in the best possible way. Opportunities for leadership development throughout an organization can be a powerful incentive to join or stay with any company.12 Rewards and opportunities for community bankers, especially in rural areas or smaller markets, typically differ from those at larger banks, but incentives that balance risk and financial results are essential to maintain the integrity of any organization.13 For example, aggressive employee bonus programs tied solely to loan growth fail to emphasize the importance of credit quality, and, in turn, a bank is rewarding employees on only one performance factor, which could lead to extending loans that do not adhere to proper underwriting standards.

The Diversity Paradigm

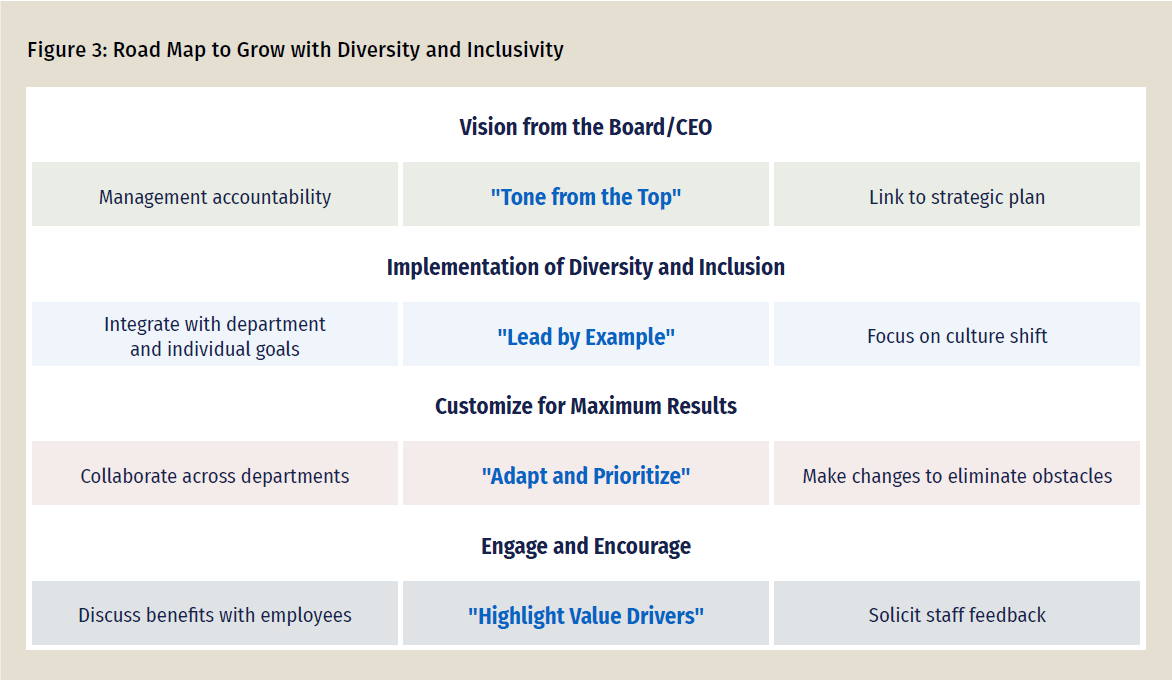

A bank’s succession plan should consider the positive impact of diversity in its leadership team on the organization. According to the Diversity of Thought study conducted by global executive search firm Heidrick & Struggles, surveying more than 230 senior board members from the top 400 publicly listed companies, 97 percent of high-ranking executives believe that diversity of thought is among the most important goals when leading successful companies.14 When determining the optimal composition of leadership, it is appropriate to be wary of “groupthink,” which characterizes how members of a leadership team with similar backgrounds tend to align in thought and gravitate to the same strategies. Team diversity slows the progression to groupthink by providing more capacity for alternative viewpoints.15 As noted in Figure 3, linking diversity to growth strategy ensures that value drivers16 are enabled and initiatives are properly prioritized, as a diverse group will more likely reevaluate information and remain even-handed.

Research conducted by McKinsey & Company17 has confirmed a correlation between financial performance and executive teams with gender, ethnic, and cultural diversity. Organizations in the top quartile for gender-diverse executive teams were 21 percent more likely to outperform on profitability and 27 percent more likely to have superior value creation. Organizations in the top quartile for ethnically and culturally diverse executive teams were 33 percent more likely to have industry-leading profitability. Organizations in the bottom quartile for both gender and ethnic/cultural diversity were 29 percent less likely to achieve above-average profitability than all other organizations in the data set. The real challenge for any workplace is to acknowledge the business sense of embracing the core philosophy of diversity. Ultimately, management teams infused with diverse backgrounds and credentials have the ingredients for spurring robust discussion, considering innovation, and ensuring thorough decision-making.18

Observed Practices

Management succession practices vary, depending on each institution’s asset size and complexity, risk profile and appetite, business model, culture, management talent, and other operational considerations. In discussions with banks supervised by the Federal Reserve, various practices were highlighted as effective, such as identifying employee development needs and opportunities, establishing clear job descriptions, and requesting prospective retirement timing from directors and senior management to reduce transition ambiguity. Larger community banks use additional tracking reports to identify multiple levels of candidates, skill rankings, and readiness time frames. Institutions of differing asset size also indicated that employing outside consultants to facilitate strategic planning discussions provides an independent perspective on succession tactics.

During the examination process, examiners noted that many community banks have been transparent about advancement opportunities for employees and customized development plans and established milestones to provide a career path. Some banks had clearly articulated criteria for board of directors and senior management composition, including guidance to foster diversity initiatives and underscore the importance of professional integrity. Some banks employ a personnel “depth chart” to designate interim leadership when needed as well as a “playbook” listing self-projected retirements and other foreseeable events that would result in management turnover. Bank-owned life insurance has been employed as a supplemental succession tool to offset loss and expected transition costs associated with a death of a key executive while still providing an earning asset. Banks have also accessed banking trade associations, local colleges, and other venues for identifying potential leadership candidates, while using pre-employment screening criteria to vet outside candidates.

Of course, these practices may not be “best fits” to fulfill the specific needs of every bank. However, these examples may be considered to create and maintain a tailored management succession program. Both examiners and bankers stress the importance of institutional integrity and reputation by maintaining proper staffing as the cornerstone of a bank’s standing in the local community.

Conclusion

Community bank directors, particularly those in small towns and rural areas, often comment that hiring and retaining key officers, as well as prospective successors, can be very challenging. Given the importance of maintaining qualified leadership, any significant disruption can have negative ramifications on a bank. Hence, a management succession program that is a living document nimble enough to readjust in a timely fashion to address personnel, economic, and strategic planning is an appropriate risk management tool.

Management is responsible not only for day-to-day operations of the bank and the quality of its assets but also for planning for the future. Since a direct relationship exists between the overall condition of a bank and the capability of management, the first priority for any examiner when evaluating the condition of a bank is to make an accurate appraisal of the management team. This supervisory assessment should include an understanding of the board of directors’ plans to provide for future bank leadership.

Effective succession planning and management is crucial to the ongoing viability of any organization. To reiterate Governor Bowman’s stance on the contribution of community banks, “One factor is the vital leadership and supporting role many small banks play in their communities. While that benefit may be hard to measure, I think it is essential that researchers try to do so. Communities need leaders and institutions that are deeply rooted in their cities, towns, and rural areas. Strong relationships and extensive experience are not easily replaced.”19

- 1 The survey report is available at www.bankdirector.com/wp-content/uploads/2019_Compensation_Report.pdf.

- 2 See Emily McCormick, “2019 Survey Results: CEO and Board Pay Trends,” June 17, 2019, BankDirector.com, available at www.bankdirector.com/committees/compensation/2019-survey-results-ceo-and-board-pay-trends/.

- 3 Read Governor Bowman’s October 1, 2019, speech, “Advancing Our Understanding of Community Banking,” at the 2019 Community Banking in the 21st Century research and policy conference held in St. Louis, available at www.federalreserve.gov/newsevents/speech/bowman20191001a.htm.

- 4 See Supervision and Regulation (SR) letter 96-38, “Uniform Financial Institutions Rating System,” December 27, 1996, available at www.federalreserve.gov/boarddocs/srletters/1996/sr9638.htm.

- 5 See the FDIC’s Supervisory Insights, Special Corporate Governance Edition, April 2016 (revised October 2018), available at www.fdic.gov/regulations/examinations/supervisory/insights/sise16/si-se2016.pdf.

- 6 See the OCC’s Comptroller’s Handbook: Corporate and Risk Governance, version 2.0, July 2019, available at www.occ.gov/publications-and-resources/publications/comptrollers-handbook/files/corporate-risk-governance/pub-ch-corporate-risk.pdf.

- 7 See David V. Day, Developing Leadership Talent: A Guide to Succession Planning and Leadership Development, 2007, SHRM Foundation, available at www.shrm.org/hr-today/trends-and-forecasting/special-reports-and-expert-views/Documents/Developing-Leadership-Talent.pdf.

- 8 See SR letter 16-11, Attachment, “Supervisory Guidance for Assessing Risk Management at Supervised Institutions with Total Consolidated Assets Less Than $100 Billion,” February 17, 2021, available at www.federalreserve.gov/supervisionreg/srletters/sr1611.htm.

- 9 See Basics for Bank Directors, a publication issued by the Federal Reserve Bank of Kansas City, Division of Supervision and Risk Management, available at www.kansascityfed.org/banking/basics-bank-directors/.

- 10 See SR letter 16-11, Attachment.

- 11 See Supervisory Insights, Special Corporate Governance Edition, April 2016.

- 12 See Day, Developing Leadership Talent, 2007.

- 13 See “Guidance on Sound Incentive Compensation Policies,” Federal Register, Volume 75, No. 122, June 25, 2010, available at www.govinfo.gov/content/pkg/FR-2010-06-25/pdf/2010-15435.pdf.

- 14 See Gabriella Jozwiak, “’Diversity of Thought’ Highly Important When Hiring Boardroom Talent,” HR magazine, February 27, 2014, available at www.hrmagazine.co.uk/article-details/diversity-of-thought-highly-important-when-hiring-boardroom-talent.

- 15 See Anna Johansson, “Why Workplace Diversity Diminishes Groupthink and How Millennials Are Helping,” Forbes, July 20, 2017, available at www.forbes.com/sites/annajohansson/2017/07/20/how-workplace-diversity-diminishes-groupthink-and-how-millennials-are-helping/#42b695e74b74.

- 16 “A value driver is an activity or capability that adds worth to a product, service, or brand. More specifically, a value driver refers to those activities or capabilities that add profitability, reduce risk, and promote growth in accordance with strategic goals.” See “Value Driver,” Whatis.com, available at https://whatis.techtarget.com/search/query?q=value+driver.

- 17 See Vivian Hunt, Lareina Yee, Sara Prince, and Sundiatu Dixon-Fyle, “Delivering Through Diversity,” January 18, 2018, McKinsey & Company, available at www.mckinsey.com/business-functions/organization/our-insights/delivering-through-diversity.

- 18 See David Rock and Heidi Grant, “Why Diverse Teams Are Smarter,” Harvard Business Review, November 4, 2016, available at https://hbr.org/2016/11/why-diverse-teams-are-smarter.

- 19 Governor Bowman, “Advancing Our Understanding of Community Banking,” October 1, 2019.